Buy Now, Pay Later Is Starting to Look Like Financial Glitter

Micheal C.May 26, 2026 4 min read

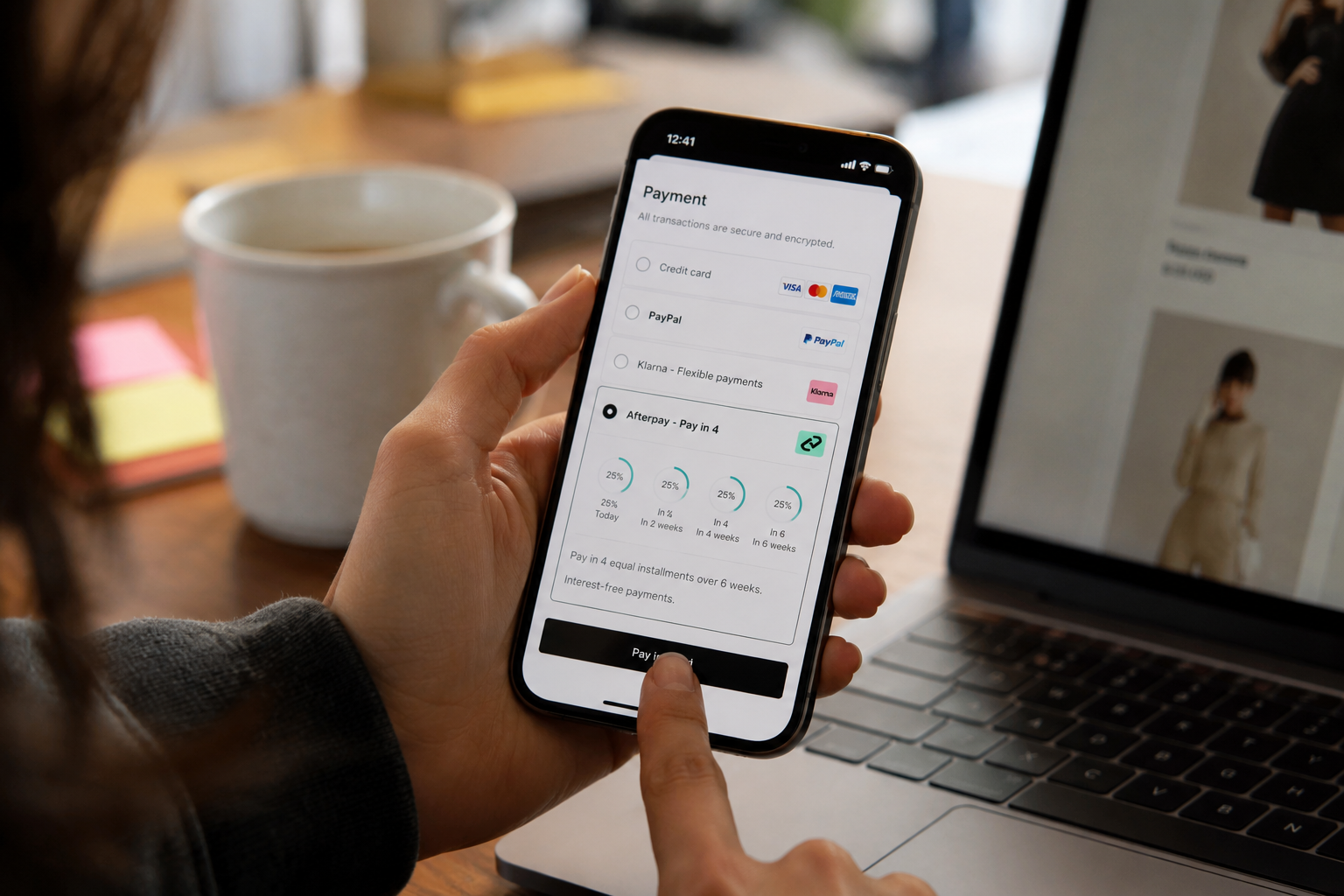

The most dangerous phrase in personal finance might not be “market crash” or “credit card debt.” It might be four tiny words that sound almost innocent: pay in four installments. Cute. Soft. Friendly. The checkout page basically whispers, “Relax, babe, this is not a real purchase, it is just four little financial vibes.” And that is exactly why Buy Now, Pay Later has become such a sneaky monster.

BNPL did not arrive looking scary. It arrived looking modern. It made old-school credit cards feel dusty, like something your parents used at a department store in 2009. Instead of one big ugly charge, BNPL sliced purchases into smaller pieces that felt easier to justify. The $220 jacket became “only $55 today.” The skincare cart became “basically nothing right now.” The concert outfit became “future me will handle it.” And honestly, that is where the trap gets good, because future you is already tired, already paying rent, and absolutely not thrilled to meet past-you’s little purchases.

The trend is very real. A 2026 finance piece reported that 59% of Gen Zers use BNPL deals, and among those users, 57% had missed a payment as of early 2026, based on LendingTree data. Another May 2026 report said 49% of Gen Z consumers planned to use BNPL for large purchases, while 36% expected to use it for daily essentials like groceries and gas. That last part is the real alarm bell. Financing a sofa is one thing. Financing groceries means the economy has started handing people duct tape and calling it innovation.

This is why BNPL feels like financial glitter. It makes everything look better for a second, then suddenly it is everywhere and impossible to clean up. One installment is manageable. Three are annoying. Seven are chaos with branding. The real problem is not that people are dumb with money. That take is lazy and, honestly, boring. The problem is that modern life is expensive, wages feel stretched, social media turns every ordinary week into a lifestyle competition, and checkout pages have become extremely good at making debt feel like self-care.

There is also a tracking problem. PYMNTS reported in March 2026 that 56% of Gen Z users said they struggle to track when store-card installment payments are due, while 47% said the same about credit card installment payments. That is not shocking. Most people do not live inside a spreadsheet. They live inside rent, food, subscriptions, birthdays, group dinners, emergency Ubers, and the weird little purchases that happen when life feels annoying. BNPL thrives in that mess because it does not feel like one big decision. It feels like a bunch of tiny ones hiding in different apps.

And this is where finance gets emotional, whether people admit it or not. Spending is rarely just math. Sometimes it is boredom. Sometimes it is loneliness. Sometimes it is wanting to look like the version of yourself you are still trying to become. Sometimes it is buying the thing because your life feels stuck and the package arriving on Thursday gives you one clean little moment of control. We can pretend money is purely rational, but anybody who has bought something at midnight knows that is a beautiful lie.

The smarter move is not to shame people out of BNPL. That never works. The smarter move is to treat it like spicy food: not evil, but you better respect it. BNPL is fine when the purchase is planned, the money is already there, and the installment schedule does not collide with rent, groceries, or actual life. It becomes dangerous when it is used to make unaffordable things feel temporarily affordable. That is not convenience. That is a financial jump scare with better UX.

So maybe the new money flex is not pretending to be rich online. Maybe it is being annoyingly clear with yourself before you tap the button. Can I buy this in full today? Will I still want it after 24 hours? Do I already have three payments coming out next week? Am I buying this because I need it, or because my brain wants a tiny reward for surviving capitalism? Brutal questions, yes. Useful ones too.

BNPL is not going away. It is too smooth, too profitable, and too perfectly designed for the way people shop now. But that does not mean it gets to quietly turn every paycheck into a group project. The real win is knowing the difference between a tool and a trap. Because paying later sounds cute until later pulls up with receipts.

Be the first to like this article

Comments (0)

0/2000

No comments yet. Be the first to share your thoughts!

Share this article

Found this helpful? Spread the word.